AI Evolution in Crypto

Decentralized Computing and Price Oracle Providers to Benefit?

This piece was a private report published on 7 June, 2023 and is now made public for readers of the newsletter. As of the time of publishing, I do not hold a position in any of the tokens mentioned in this report.

AI Tooling Fuels Demand for Data

The rise of AI, particularly in the Web3 sector, presents potential opportunities for investment. This is largely driven by the increasing demand for vast volumes of data, both historical and real-time, by AI models. The crypto market is an inefficient one and closing inefficiencies is exactly what AI tooling does best. Thus, I foresee the number of AI tools such as portfolio management, LP management, and trading vaults/bots increasing rapidly in the coming months.

As a result, demand for data will increase and data providers such are poised to reap considerable benefits, particularly those that offer API services, furthering the potential value creation within the space. I spoke to Coingecko — they reported that their API business has grown by “10x over the last 2 years”, underscoring the robust demand for their offerings. In fact, CoinGecko confirmed that “more CG API users are experimenting with AI-related projects by leveraging our data”.

However, most data providers like CoinGecko are privately held, limiting any sort of investment opportunities to private rounds, if any.

Infrastructure and Oracle Providers Present Indirect Investment Opportunities

Although direct investment avenues are limited, there is untapped potential in looking at this from a different perspective. The projected expansion of web3 data providers results in corresponding growth in infrastructure services that support both API businesses and AI tooling. However, most popular infrastructure companies are off-chain and already trillion-dollar tickers such as AMZN, GOOGL, and MSFT (note that these also service non-crypto AI tooling and thus have a huge TAM). Looking on-chain, potential beneficiaries could be decentralized computing providers such as Render Network and Akash, as well as price oracles and services like Chainlink, Filecoin, etc.

For the purpose of this report we will zero in on:

Decentralized Computing Providers (RNDR & AKT)

Price Oracle Protocols (LINK, BAND, UMA, & DIA)

Decentralized Computing Providers

Render Network (RNDR)

Render Network (RNDR) is a decentralized peer-to-peer network on the Ethereum and Polygon blockchains (they are soon migrating to Solana) that allows users to rent out GPU computing power. RNDR primarily focuses on providing GPU power for 3D rendering services for popular render engine OctaneRender. They have recently added integration for Stable Diffusion image renders and have indicated future support for LLM models.

In its current state, there is no flow of revenue to the RNDR Foundation nor its token holders. However, this is being addressed with the upcoming BME model (RNP-002) and an imposed 5% network fee on all transactions. Some quick math: as of the time of writing, RNDR is trading at $2.3. Taking RNDR usage in 2022 of 1.85 million, 5% of this represents an annualized revenue of around $212,750. Note that this would be revenue to the RNDR Foundation and not to token holders. Token holders may benefit from RNDR being potentially deflationary due to the new BME model.

Akash (AKT)

Akash (AKT) is a decentralized marketplace for cloud computing resources.

Akash recently started developing AkashAI, a decentralized network of GPUs specifically for hosting LLMs.

New tokenomics being tabled for AKT that will help to better incentivize node providers to increase supply of computing resources, as well as distribute a share of network revenue to stakers.

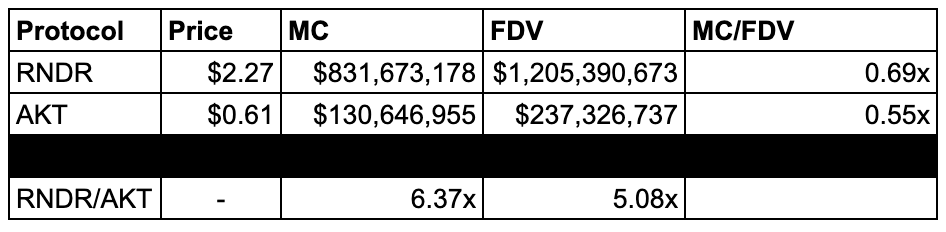

Comparing RNDR & AKT

AKT is significantly undervalued compared to Render Network (RNDR), up to 6x in terms of market capitalization — its venture into an AI-focused GPU network is recent, thus the market might not have sufficiently priced this in yet, which results in opportunity for potential upside.

Further research has to be done to determine its potential to compete against Render Network in terms of GPU demand.

Oracle Providers

Price oracle providers like Chainlink (LINK), Band Protocol (BAND), and Uma (UMA, might benefit from increased demand in AI tooling. These services act as the bridge between on-chain and off-chain data, delivering reliable, real-time data to smart contracts on the blockchain. Given the expected growth of data demands, especially real-time price feeds, oracle providers stand to benefit significantly as well.

Source: DefiLlama (data as of Jun. 7th, 2023)

As per DefiLlama, the oracle provider sector secures a total value of $28.8 billion. Chainlink is the largest oracle provider in terms of both total value secured (TVS) and number of protocols served, capturing more than 46% of the TVS market share. Other notable providers include Pyth Network, Band Protocol, DIA, and Uma. It is interesting to note that due to the importance of price oracles to ensure assets are accurately priced, e.g. on lending protocols (to avoid surprise liquidations), these typically rely on more than one oracle provider, resulting in shared market space. However, the space remains a competitive one – of the 44 oracle providers listed on DefiLlama, only five oracle providers have customers in the double digits (from the images above, “TWAP” and “Internal” refer to a method of oracle pricing as opposed to an actual oracle provider).

Valuation Comparison

Source: CoinGecko, DefiLlama (data as of Jun. 7th, 2023)

Chainlink (LINK), the leading player in the space, is priced at $6.20 and has a market cap of roughly $3.2 billion and a fully diluted valuation (FDV) of $6.2 billion. It secures 303 protocols with a total value secured (TVS) of $13.26 billion. This gives LINK a MC/TVS ratio of 0.24x and a FDV/TVS ratio of 0.47x, reflecting relatively lower valuation ratios given its secured value.

Band Protocol (BAND) is priced at $1.29, with a market cap of around $162.8 million and an FDV of $174.1 million. BAND secures 24 protocols and has a TVS of $229.61 million. Its MC/TVS ratio is 0.71x and its FDV/TVS ratio is 0.76x. While BAND has the lowest FDV/MC ratio of the lot, note that token supply is inflationary.

UMA (UMA), priced at $1.79, has a market cap of $128.8 million and an FDV of $204.7 million. It secures 8 protocols and has a TVS of $65.14 million. Its MC/TVS ratio of 1.98x and FDV/TVS ratio of 3.14x are both significantly higher than Chainlink and Band Protocol.

DIA (DIA) is priced at $0.27, with a market cap of $25.6 million and an FDV of $54.3 million. It secures 27 protocols and has a TVS of $111.21 million. DIA has an MC/TVS ratio of 0.23x and a FDV/TVS ratio of 0.49x.

Pyth Network (no token yet), secures 68 protocols and has a TVS of $1.2 billion, currently does not have available pricing or valuation data. Has already closed three private funding rounds, amount raised and valuations were undisclosed.

From the above, both LINK and DIA appear to be relatively undervalued in terms of TVS compared to their respective market caps. However, LINK particularly stands out due to its superior value accrual and market dominance. The DIA token has no other utility than for governance – no revenue is shared with token holders, although tokens can be (and have been) burned via governance.

On the other hand, LINK’s introduction of staking, despite being capped at the moment, allows LINK stakers to earn staking rewards. As of the time of writing, community stakers (non-node operators) earn a flat rate of 4.75% (100% from an incentivization program). While only node operators currently earn a share of network revenue from user fees, community stakers will begin to earn a share of revenue in future versions of Chainlink Staking. Thus, with increased demand stemming from the AI evolution and new staking mechanics on the horizon, LINK presents an interesting opportunity.

Updated (25 July, 2023): Chainlink recently announced the launch of its Cross-Chain Interoperability Protocol. This is a significant development as this adds a significant source of revenue to the Chainlink protocol due to its large network and potential for integration with a wide range of protocols, both crypto-native and institutional.

My personal picks to watch from both categories are AKT and LINK:

Thesis Summary

Increase in Web3-based AI tooling has resulted in an increase in demand for API services that provide both historical and real-time on-chain data, such as price feeds, token information, etc. CoinGecko has confirmed that their CG API users have been experimenting with AI-related projects.

CoinGecko reported a 10x growth in their API business over the last two years, while DefiLlama reported a “constant growth” in the same period, despite the overall crypto markets performing poorly. However the opportunity for investments in this category remains limited to private rounds, if any.

The uptick in demand for on-chain data should also benefit auxiliary sectors such as decentralized infrastructure providers and price oracle providers.

Akash Network (AKT) is significantly undervalued compared to Render Network (RNDR), up to 6x in terms of market capitalization as it seems that the market has yet to price in its recent venture into a GPU-network focused on hosting LLMs.

Chainlink (LINK) is relatively undervalued compared to its peers given the amount of value secured compared to its market cap. Furthermore, LINK’s tokenomics update ensures that any upside in revenue captured from future increased demand will be passed on to LINK stakers. This is unlike its competitors, as most other oracle provider tokens have no utility other than governance. The launch of CCIP adds a significant source of revenue to the protocol. With staking launching soon (hopefully EOY), this will introduce a supply sink, reducing circulating LINK so long as the protocol continues to generate revenue.

Updated (25 July, 2023): The more I think about it the more I feel that AI’s role in LINK’s upside may not be as significant as I thought, however, the above are significant enough catalysts for LINK.

Risks

AKT

AKT’s services are priced and denominated in AKT. This represents a significant UX barrier for non-crypto users. RNDR on the other hand provides a credit system for users to pay for services in fiat (USD).

AKT’s lack of mind-share compared to RNDR may see it fail to gain any sort of traction in both the supply (node operators) and demand (users) sides of its network.

The market may have overvalued RNDR (only ~$200k annualized revenue in 2022), thus making AKT fairly priced.

LINK

Developers may favor off-chain price feeds such as DefiLlama and CoinGecko in the development of AI tooling compared to on-chain oracles.

Delays in the launch of Chainlink Staking for the mass public may discourage investors due to the lack of value accrual to non-node operator stakeholders.

The oracle provider sector is a competitive one. Whilst there are no competitors that come close in terms of TVS, market dominance, and favourable tokenomics — the shared market dynamics of the space continues, thus the threat of competition remains.

Disclaimer

The content provided in this report is for informational purposes only and does not constitute financial advice. The author is not responsible for any decisions made based on the information provided herein. The opinions, analyses, and information included are based on the author's perspective and while believed to be accurate, should not be relied upon without conducting your own research and due diligence. The author may or may not be invested in any of the projects or tokens mentioned in the newsletter.

Additionally, the views and opinions expressed in this report are those of the author alone and do not reflect the views, policies, or positions of any organizations the author is affiliated with or contributes to.

It is always advisable to consult with a qualified professional before making any financial decisions. All investments involve risks, including the potential loss of principal.